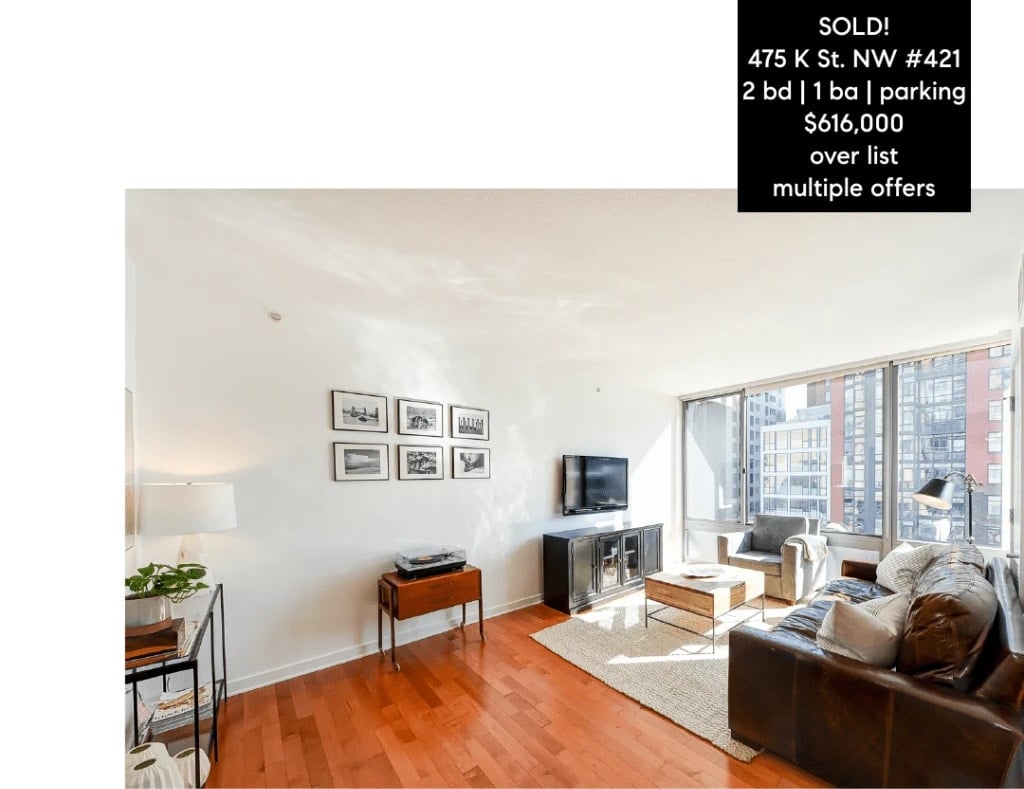

It’s official..the DC real estate season has started. The Super Bowl is over, the weather is temperate and buyers are swarming. Listings in the hot neighborhoods are going under contract quickly and multiple offers are still a reality. Interested in buying but have no idea where to start? I’ve pulled together a cheat sheet for you.

Talk to a lender.

Picking a competent lender is the most important step in the buying process. Obtaining a loan is difficult these days. Your credit has to be good. You debt to income ratio has to be just right. Lenders need reams of documentation. Stay away from the big banks. Work with someone who’s local and knows the market. Once you’ve spoken to a lender and they have all the info they need (bank statements, salary stubs, financial records, your credit score. it’s invasive. get ready.) you’re pre-qualified and ready to start searching.

Find a property.

Discovering real estate you want to purchase involves looking at listings online and visiting houses/condos/coops. A picture can only convey so much. It’s wise to visit as many properties as possible to determine what appeals to you. The search can take a day or several months.Make an offer.

Once you find a property you love, write an offer. The DC market is competitive which means you’ll need to make quick decisions. If a listing is priced well, looks good and is in a desirable location, it’s going under contract in 1-7 days and often has multiple offers.Execute the paperwork.

After your offer has been reviewed and ratified, the contract is sent to the lender and the title company. The title company reviews the title work. Their job is to make sure the property is delivered with a clear title. The lender starts processing your loan and orders the appraisal.Fulfill the contingencies (if there are any).

With the increase in multiple offers, contingencies have been on the decline. If the sellers accept an appraisal, financing or home inspection contingency, fulfill them. If they go smoothly, you’ll head to closing.Execute the final reviews.

Before closing, you do a final walk through to see if the property is still in good shape. You will also review the CD (the closing document) 3 days before closing to make sure all your fees are correct. If everything is in order, you sign the closing documents at the closing table.Complete the documents.

Once all the documents are signed, you’re a proud homeowner. Congratulations!The entire process making an offer; its acceptance, ratification, expiration of any contingencies to closing usually takes 30-45 days. The days till closing starts the day you submit the offer to the listing agent. The closing date is usually 30-45 days from the date the contract is written.

A few definitions: means when all parties (the seller and buyer) agree to the terms of the contract. There are lots of variables to an offer. All terms stated in the contract are negotiable points: the price, the closing date, how many days you have for your home inspection, financing contingency and appraisal contingencies. Once ALL the negotiating points have been agreed upon, the contract is ratified.

are a fulfillment of a condition. There are 3 contingencies that are normally used in a contract that protect the buyer: the home inspection, financing and appraisal contingencies. All 3 of these contingencies have to be met before you can close on a property if they’re included in the contract. There are different reasons to have these contingencies. Essentially, they protect the buyer from losing their earnest money deposit. As I mentioned above, these contingencies are used less frequently as the market becomes more competitive.

An earnest money deposit (EMD) is the deposit that the brokerage or title company holds in an escrow account. It goes towards your closing costs. The earnest money deposit is usually 3-5% of the offer price. It’s not deposited into the escrow account until the contract is ratified. If the contract is not ratified, the EMD monies are returned to you.

Closing costs in DC run about 3% of the purchase price. The two biggest costs covered by the 3% is the title insurance and the recordation tax that goes to DC Gov. This tax is 1.45% of the purchase price over 400K and 1.1% of the purchase price under 400K. For 2017, DC passed a first time home buyers tax break and the recordation fee is .0725% on all properties.

While buying a home can be a stressful, the end result is worth it. You own a home! 2017 is shaping up to be a wonderful time to buy while interest rates remain low and the first time home buyers tax break is in effect. Ready to buy this year? Contact me via email or phone ([email protected]/202-285-4238) and we’ll get started!